Although we've had lots of rain here over the Christmas holiday, the sun is now shining in New Bern, and we're looking forward to dryer weather.

December temperatures in the 60's is just fine with me! ;-)

Wishing everyone a very happy and healthy 2007!

Tuesday, December 26, 2006

Tuesday, December 05, 2006

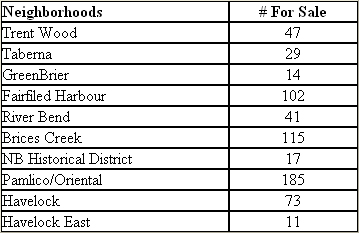

Local New Bern News - Market Update

This column is customized each month so that I can share with you, the current monthly statistics.Please feel free to contact me if you have any questions! ddunn@dunn.com

HOMES SOLD (Closed), November 1 through November 30. (From NB Board of Realtors MLS System)

Under $100K = 17

$100K-$159,999 = 65

$160K-$199,999 = 20

$200K-$239,999 = 20

$240K-$299,999 = 12

$300K-$399,999 = 7

$400K - $499,999 = 6

Over $500,000 = 6

Total = 153

Neighborhood - SALES:

Neighborhood - FOR SALE:

For the BEST Internet Marketing, and the Most Responsive Service in New Bern, Contact DIANNE! ddunn@dunn.com (252) 636-3301 or Toll Free: (888) 781-8800

Friday, December 01, 2006

New Waterfront Projects in New Bern, NC!

Two new projects in New Bern, North Carolina on the Neuse River:

1. River Station: Waterfront and waterview homesites, 17 total, located in the beautiful Historic District, with private marina. Prices from $199,900.

2. Harbour View: Waterview Townhomes with elevator options. Located in Fairfield Harbour, featuring a 265 Slip Marina, 2 Golf Courses, Fitness Center, Indoor and Outdoor Pools, Tennis courts and waterside dining. Prices fro $295,000.

For more information, you can contact me from my website: www.NewBernHomes.com or call me Toll Free at 888-781-8800

Monday, November 27, 2006

Keeping Your Credit Clean

Many homebuyers frequently wonder, "If I am shopping for a home loan will my credit be affected each time a credit report inquiry is made?"

It's a logical and intelligent question to ask; the answer is: not significantly, if the credit checks are done in a short period of time.

When a credit check is made by a potential lender it is called a hard inquiry. When a hard inquiry occurs it does have an impact on your credit score. However, when you're shopping for a mortgage or a car loan, credit bureaus typically cluster the hard inquiries together because the credit reporting bureaus understand that the consumer is shopping for the best loan.

"So for example, if you're shopping for a new mortgage and three potential lenders pull your credit score within three weeks, that is looked at as one inquiry for that purpose," says Steven Katz a spokesperson for TransUnion's TrueCredit.com. Keeping your credit clean is critical. Katz offers the following advice to help ensure healthy credit.

"If at all possible, people should have a locking mailbox," says Katz. Katz says mailboxes with locking devices are becoming more popular at hardware stores because identity theft is spreading. Taking precaution to protect your personal information can save you months of agony.

Shred your documents: Katz says if you don't shred your personal documents and criminals access the information, the result can be devastating to your credit.

Keep an eye on your credit card: Katz says while it is difficult, people should not let their credit card out of their sight or else they run the risk of becoming a victim of skimming. Skimming has become prevalent at some restaurants and gas stations where a clerk might have a small device that scans the consumer's credit card. "It's a very small scanner that captures all the information that is on the magnetic strip, and then the card's information can be cloned," explains Katz.

Be sure to keep all credit card receipts, and Check your credit history:

Consumers can check their credit history for free once a year at http://annualcreditreport.com. Katz says that the free reports will not contain an actual credit score, but you can get the scores for a fee.

Another good credit-checking resource is found at http://truecredit.com. The website offers access to tools to manage a consumer's credit health by receiving credit reports, credit scores, credit monitoring, and informational materials.

Edited by Dianne Dunn, from original writing by Phoebe Chongchua

Friday, November 10, 2006

Seller's Home Appeal for Today's Market

After years of hearing from successful sellers that they didn't have to do a thing to sell, they now need to understand how they can stand out from their competition. Here is a handy list to help sellers determine if some features in their home might need some attention.

Test all door and cabinet knobs. Replace mismatched or inexpensive hardware for a quick update. Buyers rarely can get beyond a knob that comes off in their hand as they attempt to use a door.

Take the time to paint walls, trim and ceilings. Keep adjoining rooms in one color palette, which will make your home appear larger. Clean up spills from messy painters. Hire professionals to paint mullions on windows and staircase spindles.

Slipcover mismatched furniture in a room that requires visual unification.

Discover ways to organize day-to-day room needs. Substantial wicker baskets or square stainless steel or brass containers can organize magazines, remote controls and toys. Books provide a good look, but vary them by laying some down and standing some up.

Wallpaper is considered fill-in-the-blank decorating. No two people have the same taste in this instant decorator wannabee. If it's more than three years old, take it down and paint in a neutral color. And wallpaper borders are out.

Simple furniture rearrangement can bring new life to a tired space. Float sofas and coffee tables away from walls for a designer look. Use area rugs to anchor furniture groupings on bare tile and wood floors. Place groupings of candles and clear glass bowls filled with natural potpourri, fresh fruit or glass crystals on side and coffee tables.

Make sure there is balanced lighting in every room for dusk and evening showings. Dimmers help set the right tone.

Polish and wax hardwood floors to brighten and blend an old finish.

Clean every surface until it shimmers and shines. Clean can seal a deal. Don't forget the windows.

Purchase the best quality carpet pad which can make any new carpeting "cushy," and home buyers love cushy. Stay away from shag styles; buyers know it won't be around long in style cycles.

Streamline window fashions. Heavy drapes are in the minority. Think "let the light shine in" when placing blinds and shades. Light and bright can overcome other issues with a home.

Freshen-up closets with closet organizers to maximize storage space and paint a neutral, washable color. Thinning closets, cabinets, basements, attics and garages will also help your storage spaces look larger. If you can't part with items, rent a storage locker to hold items for decision making later.

Don't forget the basement; dark, dirty and musty basements are a turn-off to buyers. Add extra lighting, paint the floor and vacuum out all the cobwebs. Organize storage areas and take the time to clean the washing machine and dryer. To spruce up the hot water heater and furnace, wipe down with a strong cleaner. Scrub the laundry tub and sweep left-over leaves out of exterior stairs and window wells. Run a dehumidifier to reduce basement moisture.

Take a good look from the street or road at the front of your home. Look for shrubs that are overgrown or dead and remove and replace them with shrubs or plants that are to scaled to your home. Small inexpensive bushes send the wrong message.

Limit yard ornaments to a favored few. Excess ornaments can make yards look busy and buyers might want them included in a purchase contract.

Paint and refresh yard lights, flagpoles, mailboxes, window boxes, fences and trellis. Don't forget the swing set or play equipment.

Replace broken bricks on terraces, cracked concrete patios and steps.

Restore screens on porches and lanai's. Dirty, rusty and ripped screens limit functionality to homebuyers.

Don't leave pets unattended for property showings, especially if you think they could be aggressive or territorial around strangers.

Have carpets and area rugs cleaned before showing your home to potential buyers. Those allergic to animal dander and hair, even if they can't see your pet will know when their eyes and nose start to alert them to an allergic reaction. Many will not purchase a home that poses strong allergy issues.

A barking dog or overly-friendly cats can kill a showing. Be pro-active and take your pets off site for showings. Hire a dog walker to occupy pets if you can't be home.

Written by Mark NashBullet

Test all door and cabinet knobs. Replace mismatched or inexpensive hardware for a quick update. Buyers rarely can get beyond a knob that comes off in their hand as they attempt to use a door.

Take the time to paint walls, trim and ceilings. Keep adjoining rooms in one color palette, which will make your home appear larger. Clean up spills from messy painters. Hire professionals to paint mullions on windows and staircase spindles.

Slipcover mismatched furniture in a room that requires visual unification.

Discover ways to organize day-to-day room needs. Substantial wicker baskets or square stainless steel or brass containers can organize magazines, remote controls and toys. Books provide a good look, but vary them by laying some down and standing some up.

Wallpaper is considered fill-in-the-blank decorating. No two people have the same taste in this instant decorator wannabee. If it's more than three years old, take it down and paint in a neutral color. And wallpaper borders are out.

Simple furniture rearrangement can bring new life to a tired space. Float sofas and coffee tables away from walls for a designer look. Use area rugs to anchor furniture groupings on bare tile and wood floors. Place groupings of candles and clear glass bowls filled with natural potpourri, fresh fruit or glass crystals on side and coffee tables.

Make sure there is balanced lighting in every room for dusk and evening showings. Dimmers help set the right tone.

Polish and wax hardwood floors to brighten and blend an old finish.

Clean every surface until it shimmers and shines. Clean can seal a deal. Don't forget the windows.

Purchase the best quality carpet pad which can make any new carpeting "cushy," and home buyers love cushy. Stay away from shag styles; buyers know it won't be around long in style cycles.

Streamline window fashions. Heavy drapes are in the minority. Think "let the light shine in" when placing blinds and shades. Light and bright can overcome other issues with a home.

Freshen-up closets with closet organizers to maximize storage space and paint a neutral, washable color. Thinning closets, cabinets, basements, attics and garages will also help your storage spaces look larger. If you can't part with items, rent a storage locker to hold items for decision making later.

Don't forget the basement; dark, dirty and musty basements are a turn-off to buyers. Add extra lighting, paint the floor and vacuum out all the cobwebs. Organize storage areas and take the time to clean the washing machine and dryer. To spruce up the hot water heater and furnace, wipe down with a strong cleaner. Scrub the laundry tub and sweep left-over leaves out of exterior stairs and window wells. Run a dehumidifier to reduce basement moisture.

Take a good look from the street or road at the front of your home. Look for shrubs that are overgrown or dead and remove and replace them with shrubs or plants that are to scaled to your home. Small inexpensive bushes send the wrong message.

Limit yard ornaments to a favored few. Excess ornaments can make yards look busy and buyers might want them included in a purchase contract.

Paint and refresh yard lights, flagpoles, mailboxes, window boxes, fences and trellis. Don't forget the swing set or play equipment.

Replace broken bricks on terraces, cracked concrete patios and steps.

Restore screens on porches and lanai's. Dirty, rusty and ripped screens limit functionality to homebuyers.

Don't leave pets unattended for property showings, especially if you think they could be aggressive or territorial around strangers.

Have carpets and area rugs cleaned before showing your home to potential buyers. Those allergic to animal dander and hair, even if they can't see your pet will know when their eyes and nose start to alert them to an allergic reaction. Many will not purchase a home that poses strong allergy issues.

A barking dog or overly-friendly cats can kill a showing. Be pro-active and take your pets off site for showings. Hire a dog walker to occupy pets if you can't be home.

Written by Mark NashBullet

Friday, November 03, 2006

Local New Bern News

This column is customized each month so that I can share with you, the current monthly statistics.

Please feel free to contact me if you have any questions! ddunn@dunn.com

Please feel free to contact me if you have any questions! ddunn@dunn.com

HOMES SOLD (Closed), October 1 through October 31. (From NB Board of Realtors MLS System)

Under $100K = 14

$100K-$159,999 = 55

$160K-$199,999 = 24

$200K-$239,999 = 16

$240K-$299,999 = 15

$300K-$399,999 = 13

$400K - $499,999 = 3

Over $500,000 = 4

Total = 144

TABERNA HOMES SOLD (Pending)

Total: 2

Resale Homes Total: 2

$200K-$239,999 = 1

$350K-$399,999 = 1

Builder Spec Homes Total: 0

Resale LOTS Sold (Pending) = 0

TRENT WOODS SOLD (Pending)

Total: 4

$140K-$199,999 = 1

$200K-$299,999 = 1

$300K-$399,999 = 1

$400K-$459,999 = 1

GREENBRIER HOMES SOLD (Pending)

Total: 5

$200K-$299,999 = 1

$300K-$399,999 = 2

$400K-$429,999 = 2

TABERNA HOMES FOR SALE

Total: 30

Resale Homes Total: 20

$200K-$249,999 = 6

$250K-$299,999 = 4

$300K-$349,999 = 2

$350K-$399,999 = 3

$400K-$499,999 = 2

Over $500,000 = 3

Builder Spec Homes Total: 10

$300K-$399,999 = 4

$400K-$499,999 = 6

Resale LOTS For Sale Total: 6

TRENT WOODS HOMES FOR SALE

Total: 48

$140K-$199,999 = 12

$200K-$299,999 = 11

$300K-$399,999 = 7

$400K-$499,999 = 13

Over $500,000 = 5

GREENBRIER HOMES FOR SALE

Total: 13

$200K-$299,999 = 9

$300K-$399,999 = 4

For the BEST Internet Marketing, and the Most Responsive Service in

New Bern, Contact DIANNE!ddunn@dunn.com

(252) 636-3301 or Toll Free: (888) 781-8800

Friday, October 27, 2006

Coping With A Changing Mortgage Market

Coping With A Changing Mortgage Market

After rising all year, interest rates recently fell for six consecutive weeks to their lowest point since July.

Less than a year ago, experts everywhere, from the Federal Bureau of Investigations to the Federal Reserve, questioned appraised values of homes. Now, as the boom wanes, lenders are more certain mortgages are backed by accurately valued collateral.

That doesn't mean lenders aren't still going gangbusters on riskier, high-leverage loans for those who qualify even if income, employment and asset documentation aren't checked.

Along with housing market change comes mortgage market change in a symbiotic -- sometimes nightmarish -- relationship of ebbs and flows that can leave consumers tossing and turning at night.

Fortunately, for home owners and those looking to buy, the fundamentals still apply.

Sound, consistent financial behavior can be like a dose of NyQuil.

Here are some timely mortgage tips to soothe your worries and to help you sleep more soundly.

Pull your credit report. Before you shop for any credit, pull your credit report from the only federally sanctioned free service, AnnualCreditReport.com. You don't have time for surprises. Know what the lender will know before the lender knows. You may need to make changes to your credit report, housing budget or timing, depending upon what you find.

Mortgage money shop. Shop several or more lenders and loan programs, as well as title and escrow fees, online and off to get the best deal. To make the best comparison, compare all loan costs whenever possible including rates, points, brokers fees, originating fees, yield spread premiums, recording fees, title and escrow costs, everything that will wind up on the HUD-1 Settlement Statement.

Mortgage rate locks for home buys, refinancing and equity taps, are always wise, especially during market shifts. Right now, they are crucial because experts expect the upward trend in interest rates to resume.

A rate lock takes the uncertainty out of which way rates are moving or even where they are, because it's a lender's guarantee your mortgage will come with a specific interest rate, points and other terms. Get the lock in writing and lock in as many costs and terms as possible, including the lock's effective date, expiration date and any post-lock options, should the lock expire before the deal is done.

A preapproved mortgage goes hand in hand with the rate lock. Get preapproved with a bona fide, carved-in-stone preapproval that guarantees in writing a loan amount, interest rate and as much of the other loan terms as possible.

Prequalification only indicates you are creditworthy enough to obtain a loan and lets you know how much the lender is willing to lend you, which could be more than you can afford.

With a preapproval, instead of shopping around with a nebulous loan amount, you'll be shopping for a home with a mortgage and along with personal satisfaction, it will give you a negotiating edge with the seller who'd rather not deal with slouches.

For current homeowners, take control of your equity and use it wisely to boost, not bust your home value. Any equity loan, by nature, is an equity depleting loan.

Take cash out primarily for capital improvements (not all home improvements are created equal) that will help hold or improve the value of your home, especially during times of flat and falling home values.

Home equity can be a real gold mine, but you don't want to drain your mother lode.

"Taking control of your home equity means not allowing interest rates to push you into making a hasty decision," says Jim Ferriter, an executive vice president with GMAC Mortgage.

"Instead, take a deep breath, contact your mortgage professional, and carefully explore your options. In addition, consider seeking the assistance of a financial planner or tax advisor to provide additional insights about managing your home equity in light of your other personal finance decisions."

Fundamental advise is to tap your equity for well-investigated business opportunities, education and other investments that give you a return equal to or better than the cost of equity loan.

Debt consolidation can be a wise use of equity provided you plan to actually pay off the debt and close, in writing, consolidated accounts.

Consolidate debts with care and advice from MyFICO.com or other sources that can help you prevent lowering your credit score when you close too many accounts quickly.

For emergencies -- medical, job related, child birth, deaths and the like -- consider, with determined discipline, keeping a line of credit on standby. Remember, once you are out of work, lenders are less likely to grant you a line of credit.

Written by Broderick Perkins

Wondering What Your Home Is Worth? -- Let me show you.

After rising all year, interest rates recently fell for six consecutive weeks to their lowest point since July.

Less than a year ago, experts everywhere, from the Federal Bureau of Investigations to the Federal Reserve, questioned appraised values of homes. Now, as the boom wanes, lenders are more certain mortgages are backed by accurately valued collateral.

That doesn't mean lenders aren't still going gangbusters on riskier, high-leverage loans for those who qualify even if income, employment and asset documentation aren't checked.

Along with housing market change comes mortgage market change in a symbiotic -- sometimes nightmarish -- relationship of ebbs and flows that can leave consumers tossing and turning at night.

Fortunately, for home owners and those looking to buy, the fundamentals still apply.

Sound, consistent financial behavior can be like a dose of NyQuil.

Here are some timely mortgage tips to soothe your worries and to help you sleep more soundly.

Pull your credit report. Before you shop for any credit, pull your credit report from the only federally sanctioned free service, AnnualCreditReport.com. You don't have time for surprises. Know what the lender will know before the lender knows. You may need to make changes to your credit report, housing budget or timing, depending upon what you find.

Mortgage money shop. Shop several or more lenders and loan programs, as well as title and escrow fees, online and off to get the best deal. To make the best comparison, compare all loan costs whenever possible including rates, points, brokers fees, originating fees, yield spread premiums, recording fees, title and escrow costs, everything that will wind up on the HUD-1 Settlement Statement.

Mortgage rate locks for home buys, refinancing and equity taps, are always wise, especially during market shifts. Right now, they are crucial because experts expect the upward trend in interest rates to resume.

A rate lock takes the uncertainty out of which way rates are moving or even where they are, because it's a lender's guarantee your mortgage will come with a specific interest rate, points and other terms. Get the lock in writing and lock in as many costs and terms as possible, including the lock's effective date, expiration date and any post-lock options, should the lock expire before the deal is done.

A preapproved mortgage goes hand in hand with the rate lock. Get preapproved with a bona fide, carved-in-stone preapproval that guarantees in writing a loan amount, interest rate and as much of the other loan terms as possible.

Prequalification only indicates you are creditworthy enough to obtain a loan and lets you know how much the lender is willing to lend you, which could be more than you can afford.

With a preapproval, instead of shopping around with a nebulous loan amount, you'll be shopping for a home with a mortgage and along with personal satisfaction, it will give you a negotiating edge with the seller who'd rather not deal with slouches.

For current homeowners, take control of your equity and use it wisely to boost, not bust your home value. Any equity loan, by nature, is an equity depleting loan.

Take cash out primarily for capital improvements (not all home improvements are created equal) that will help hold or improve the value of your home, especially during times of flat and falling home values.

Home equity can be a real gold mine, but you don't want to drain your mother lode.

"Taking control of your home equity means not allowing interest rates to push you into making a hasty decision," says Jim Ferriter, an executive vice president with GMAC Mortgage.

"Instead, take a deep breath, contact your mortgage professional, and carefully explore your options. In addition, consider seeking the assistance of a financial planner or tax advisor to provide additional insights about managing your home equity in light of your other personal finance decisions."

Fundamental advise is to tap your equity for well-investigated business opportunities, education and other investments that give you a return equal to or better than the cost of equity loan.

Debt consolidation can be a wise use of equity provided you plan to actually pay off the debt and close, in writing, consolidated accounts.

Consolidate debts with care and advice from MyFICO.com or other sources that can help you prevent lowering your credit score when you close too many accounts quickly.

For emergencies -- medical, job related, child birth, deaths and the like -- consider, with determined discipline, keeping a line of credit on standby. Remember, once you are out of work, lenders are less likely to grant you a line of credit.

Written by Broderick Perkins

Wondering What Your Home Is Worth? -- Let me show you.

Monday, October 23, 2006

Tips for Selling in a Buyer's Market

Tips for Selling in a Buyer's Market

As the fall season brings the usual slow-down in home sales activity, many regions of the country that experienced hot sellers' markets over the summer are now seeing a change toward buyers' markets. But don't let that hamper your plans -- if you prepare properly and make the right moves, you can sell your house.

One of the first things real estate brokers and agents will encourage you to do if you're selling in a challenging market is to price your house appropriately and add appeal.

So what can you do to give your house selling appeal? For starters, you should:

Set your price competitively.

Offer incentives. If your carpet is old or outdated, offer a carpet allowance up front. If a potential buyer knows this right off the bat, they might be able to overlook the unattractive carpet - probably the first thing they'll notice when they walk in the door. Or, offer to include your appliances with the home. If you're moving into a new home, appliances may already be included, or you may be ready to upgrade. This type of offer will be especially enticing to first-time buyers who are putting most - if not all - of their available cash into their down payment and closing costs.

Offer to pay the nonrecurring closing costs - the loan appraisal, loan points, credit report, title insurance, and property inspections. This can be a major motivation to cash-strapped buyers; these costs usually run about 3 to 5 percent of the cost of the house. Depending on your market and budget situations, you may offer to pay part or all of the costs.

Get a professional home inspection before you put your house on the market. Nothing will kill your deal quicker than a buyer's inspector finding a major problem during the inspection process. Even if you reach an agreement with the buyer on who will pay how much of the repair work - or if you agree to pay all - the fact that the buyer has to wait for the repairs could put a damper on their plans, and even trigger them to break the deal, especially if there are plenty of other comparable houses on the market.

Be flexible. When you get an offer and the buyer wants to move in sooner than you'll be ready, make plans to stay in an apartment or with relatives until your new place is ready. A month or two of inconvenience will surely be worth it down the road.

Create good curb appeal. A home shopper's first impression is everything. The moment they pull up to the curb, they'll make an instant judgment. You'll want to be sure it's positive. You can begin by making sure leaves are raked up, and your shrubs and bushes are pruned. Make sure bikes and toys are out of sight.

Focus on your walls. If your walls are dirty, it will be an automatic turnoff to potential buyers. Think about touching up the paint on your walls before you put your home on the market, keeping the colors neutral and light. Save your favorite reds and greens for your next place, where you'll be staying put for awhile.

Make sure your home shows well. Get rid of all the clutter. Keep the house clean and simple. If you have a lot of knickknacks, keep them out of sight. Make sure there are no lingering pet or smoke odors. Set out some fresh flowers. Turn on some light music.

Let the light in. Open blinds and curtains so plenty of light illuminates the home's interior.

And, most importantly, be patient. Don't be too hasty in reducing your asking price. But be ready to when the time comes. You'll want to talk to your agent about how long homes are staying on the market in your neighborhood. The time to think about reducing your price is once you pass that mark.

Written by Michele Dawson

Wondering What Your Home Is Worth? -- Let me show you.

As the fall season brings the usual slow-down in home sales activity, many regions of the country that experienced hot sellers' markets over the summer are now seeing a change toward buyers' markets. But don't let that hamper your plans -- if you prepare properly and make the right moves, you can sell your house.

One of the first things real estate brokers and agents will encourage you to do if you're selling in a challenging market is to price your house appropriately and add appeal.

So what can you do to give your house selling appeal? For starters, you should:

Set your price competitively.

Offer incentives. If your carpet is old or outdated, offer a carpet allowance up front. If a potential buyer knows this right off the bat, they might be able to overlook the unattractive carpet - probably the first thing they'll notice when they walk in the door. Or, offer to include your appliances with the home. If you're moving into a new home, appliances may already be included, or you may be ready to upgrade. This type of offer will be especially enticing to first-time buyers who are putting most - if not all - of their available cash into their down payment and closing costs.

Offer to pay the nonrecurring closing costs - the loan appraisal, loan points, credit report, title insurance, and property inspections. This can be a major motivation to cash-strapped buyers; these costs usually run about 3 to 5 percent of the cost of the house. Depending on your market and budget situations, you may offer to pay part or all of the costs.

Get a professional home inspection before you put your house on the market. Nothing will kill your deal quicker than a buyer's inspector finding a major problem during the inspection process. Even if you reach an agreement with the buyer on who will pay how much of the repair work - or if you agree to pay all - the fact that the buyer has to wait for the repairs could put a damper on their plans, and even trigger them to break the deal, especially if there are plenty of other comparable houses on the market.

Be flexible. When you get an offer and the buyer wants to move in sooner than you'll be ready, make plans to stay in an apartment or with relatives until your new place is ready. A month or two of inconvenience will surely be worth it down the road.

Create good curb appeal. A home shopper's first impression is everything. The moment they pull up to the curb, they'll make an instant judgment. You'll want to be sure it's positive. You can begin by making sure leaves are raked up, and your shrubs and bushes are pruned. Make sure bikes and toys are out of sight.

Focus on your walls. If your walls are dirty, it will be an automatic turnoff to potential buyers. Think about touching up the paint on your walls before you put your home on the market, keeping the colors neutral and light. Save your favorite reds and greens for your next place, where you'll be staying put for awhile.

Make sure your home shows well. Get rid of all the clutter. Keep the house clean and simple. If you have a lot of knickknacks, keep them out of sight. Make sure there are no lingering pet or smoke odors. Set out some fresh flowers. Turn on some light music.

Let the light in. Open blinds and curtains so plenty of light illuminates the home's interior.

And, most importantly, be patient. Don't be too hasty in reducing your asking price. But be ready to when the time comes. You'll want to talk to your agent about how long homes are staying on the market in your neighborhood. The time to think about reducing your price is once you pass that mark.

Written by Michele Dawson

Wondering What Your Home Is Worth? -- Let me show you.

Monday, October 16, 2006

Real Estate News & Views

Hello, Taberna Neighbors!

What’s Happening with real estate markets around the nation and other places? The following are a few updates as of the first week of October:

A West Chester, PA-based firm says, nationwide, the median sales price for an existing home will decline in 2007 by only 3.6 percent, but that would be the first full-year decline in home prices since the 1930s' Great Depression era.

Other reports have already revealed those unsustainable double-digit home price increases of the last half decade have begun to crumble and when the smoke clears, many home prices on the coast will be cold toast, says Economy.com.

“The highest probability of price declines is in metro areas throughout California, and in and around New York City. Probabilities are nearly as high in the rest of the Northeast Corridor, many Florida metro areas, and in sundry areas in the Midwest and Mountain West," according to the report's summary.

Declines are less likely or expected to be much less severe in Texas, most of the Southeast, the Farm Belt and the Pacific Northwest.

The greatest annual decline will visit sunny Cape Coral, FL, where home prices are forecast to decline 18.6 percent from the peak price. Other large home price declines will come from Reno, NV (17.2 percent); Merced, CA (16.1 percent); Stockton, CA (15.7 percent); Sarasota, FL (14 percent); Naples, FL (13.8 percent); Tucson, AZ (13.4 percent); Las Vegas, NV (12.9 percent); Chico, CA (12.6 percent) and Fresno, CA (12.5 percent), with another 11 metros suffering double-digit, home price declines.

Of the seven states in the nation with housing that saw a more than 80 percent rate of appreciation over the 2001-2005 period, Rhode Island, which enjoyed a 94 percent rate during the period, is the last hold out. The remaining markets have experienced rapid appreciation deceleration, according to the second quarter Home Price Index by the Office of Federal Housing Enterprise Oversight.

In Canada, the mantra appears to be “I’d rather be renovating.” The time it takes to renovate a home, the inconvenience involved, and the cost of the work are all cited as 'headaches' in a recent survey of Canadian homeowners. Even so, 80 per cent of Canadians would rather renovate than move to a different house.

The New Bern area of eastern NC is experiencing much more activity this autumn, while the coastal beach areas are seeing a very slow season.

What’s Happening with real estate markets around the nation and other places? The following are a few updates as of the first week of October:

A West Chester, PA-based firm says, nationwide, the median sales price for an existing home will decline in 2007 by only 3.6 percent, but that would be the first full-year decline in home prices since the 1930s' Great Depression era.

Other reports have already revealed those unsustainable double-digit home price increases of the last half decade have begun to crumble and when the smoke clears, many home prices on the coast will be cold toast, says Economy.com.

“The highest probability of price declines is in metro areas throughout California, and in and around New York City. Probabilities are nearly as high in the rest of the Northeast Corridor, many Florida metro areas, and in sundry areas in the Midwest and Mountain West," according to the report's summary.

Declines are less likely or expected to be much less severe in Texas, most of the Southeast, the Farm Belt and the Pacific Northwest.

The greatest annual decline will visit sunny Cape Coral, FL, where home prices are forecast to decline 18.6 percent from the peak price. Other large home price declines will come from Reno, NV (17.2 percent); Merced, CA (16.1 percent); Stockton, CA (15.7 percent); Sarasota, FL (14 percent); Naples, FL (13.8 percent); Tucson, AZ (13.4 percent); Las Vegas, NV (12.9 percent); Chico, CA (12.6 percent) and Fresno, CA (12.5 percent), with another 11 metros suffering double-digit, home price declines.

Of the seven states in the nation with housing that saw a more than 80 percent rate of appreciation over the 2001-2005 period, Rhode Island, which enjoyed a 94 percent rate during the period, is the last hold out. The remaining markets have experienced rapid appreciation deceleration, according to the second quarter Home Price Index by the Office of Federal Housing Enterprise Oversight.

In Canada, the mantra appears to be “I’d rather be renovating.” The time it takes to renovate a home, the inconvenience involved, and the cost of the work are all cited as 'headaches' in a recent survey of Canadian homeowners. Even so, 80 per cent of Canadians would rather renovate than move to a different house.

The New Bern area of eastern NC is experiencing much more activity this autumn, while the coastal beach areas are seeing a very slow season.

Real Estate Outlook: Buyers Take Note

One of the country's top housing economists has come out with a new forecast and timeline for the market over the coming months - and it's got some great insights for anybody interested in real estate.

Dr. David Seiders, chief economist for the National Association of Home Builders, says that housing starts are now down by about 20 percent from levels a year ago - but that should be no surprise.

After all, he says, after years of record housing production, the market had to cool off, "We are in the midst of an inevitable adjustment following boom years when housing market activity soared to unsustainable levels. The market that emerges from the current correction will display good balance between supply and demand, and move to a sustainable trend based on solid underlying fundamentals."

How soon might the turnaround begin? Well, nobody can answer that for certain, but based on his research, Dr. Seiders believes that the end of the down cycle may only be a matter of months away - sometime next spring is a real possibility in many areas.

In the meantime, Dr. Seiders sees an upside for consumers: If you've done your homework on your local market - and you know what's sitting unsold at what price and on what size lot - this may be a very opportune time to get off the sidelines and start making offers.

One important reason why: Dr. Seiders points out that the vast majority of local markets around the country have solid underlying economic fundamentals: Housing may be soft, but - jobs are growing. Household incomes are moving up - and inflation is under control.

Unlike some earlier cyclical downturns, such as the early 1990s recession years, the correction this time around is likely to be relatively brief and not so deep - as long as mortgage rates stay where they are, about a point above historic lows. Corrections could be deeper and longer in those markets where prices got most out of sync with local incomes, but even the majority of those metropolitan areas on the West and East coasts have relatively strong employment bases this time around.

Which raises a very basic question in my mind: When just about every economist in the country is telling us that - we're in a buyer's market, but that the down cycle may not last all that long - isn't this a smart time to be actively involved in real estate, searching for deals?

Written by Kenneth Harney

Dr. David Seiders, chief economist for the National Association of Home Builders, says that housing starts are now down by about 20 percent from levels a year ago - but that should be no surprise.

After all, he says, after years of record housing production, the market had to cool off, "We are in the midst of an inevitable adjustment following boom years when housing market activity soared to unsustainable levels. The market that emerges from the current correction will display good balance between supply and demand, and move to a sustainable trend based on solid underlying fundamentals."

How soon might the turnaround begin? Well, nobody can answer that for certain, but based on his research, Dr. Seiders believes that the end of the down cycle may only be a matter of months away - sometime next spring is a real possibility in many areas.

In the meantime, Dr. Seiders sees an upside for consumers: If you've done your homework on your local market - and you know what's sitting unsold at what price and on what size lot - this may be a very opportune time to get off the sidelines and start making offers.

One important reason why: Dr. Seiders points out that the vast majority of local markets around the country have solid underlying economic fundamentals: Housing may be soft, but - jobs are growing. Household incomes are moving up - and inflation is under control.

Unlike some earlier cyclical downturns, such as the early 1990s recession years, the correction this time around is likely to be relatively brief and not so deep - as long as mortgage rates stay where they are, about a point above historic lows. Corrections could be deeper and longer in those markets where prices got most out of sync with local incomes, but even the majority of those metropolitan areas on the West and East coasts have relatively strong employment bases this time around.

Which raises a very basic question in my mind: When just about every economist in the country is telling us that - we're in a buyer's market, but that the down cycle may not last all that long - isn't this a smart time to be actively involved in real estate, searching for deals?

Written by Kenneth Harney

Monday, October 02, 2006

Local New Bern News - Market Update

This column is customized each month so that I can share with you, the current monthly statistics.

Please feel free to contact me if you have any questions! ddunn@dunn.com

Please feel free to contact me if you have any questions! ddunn@dunn.com

HOMES SOLD (Closed), September 1 through September 30. (From NB Board of Realtors MLS System)

Under $100K = 25

$100K-$159,999 = 46

$160K-$199,999 = 23

$200K-$239,999 = 21

$240K-$299,999 = 7

$300K-$399,999 = 14

$400K - $499,999 = 7

Over $500,000 = 4

Total = 147

TABERNA HOMES SOLD (Pending)

Total: 3

Resale Homes Total: 1

$200K-$239,999 = 1

Builder Spec Homes Total: 2

$240K-$299,999 = 1

$300K-$399,999 = 1

Resale LOTS Sold (Pending) = 0

TRENT WOODS SOLD (Pending)

Total: 5

$140K-$199,999 = 2

$200K-$299,999 = 2

$300K-$399,999 = 1

GREENBRIER HOMES SOLD (Pending)

Total: 1

$440K-$499,999 = 1

TABERNA HOMES FOR SALE

Total: 32

Resale Homes Total: 24

$200K-$249,999 = 7

$250K-$299,999 = 7

$300K-$349,999 = 1

$350K-$399,999 = 4

$400K-$499,999 = 3

Over $500,000 = 2

Builder Spec Homes Total: 8

$300K-$399,999 = 3

$400K-$499,999 = 5

Resale LOTS For Sale Total: 6

TRENT WOODS HOMES FOR SALE

Total: 41

$160K-$199,999 = 4

$200K-$299,999 = 11

$300K-$399,999 = 9

$400K-$499,999 = 11

Over $500,000 = 6

GREENBRIER HOMES FOR SALE

Total: 14

$200K-$299,999 = 8

$300K-$399,999 = 6

For the BEST Internet Marketing, and the Most Responsive Service in

New Bern, Contact DIANNE (252) 636-3301 or Toll Free: (888) 781-8800

Tuesday, August 08, 2006

The Housing Bubble?

We continue to hear about the "housing bubble" in different parts of the country. Those are the areas where real estate appreciation has been rapid over the past few years, and some markets are now flooded with overpriced properties.

Eastern North Carolina appears to be one of the nation's best-kept secrets for housing affordability. Although waterfront and resort properties command premium prices everywhere, Eastern NC is still considered far more reasonable than many other coastal areas.

Smaller, historic cities like New Bern, offer all of the amenities of year-round living, while only 30 miles west of the Atlantic.

Eastern North Carolina appears to be one of the nation's best-kept secrets for housing affordability. Although waterfront and resort properties command premium prices everywhere, Eastern NC is still considered far more reasonable than many other coastal areas.

Smaller, historic cities like New Bern, offer all of the amenities of year-round living, while only 30 miles west of the Atlantic.

Subscribe to:

Comments (Atom)

{kind=link}